Report to clients for the quarter ending September 30, 2019

To date in 2019 equities have turned in their best performance for U.S. stock markets since 1997, quite an amazing result given a drumbeat of market-threatening news: tariff wars, major damage to Saudi oil production and likely impeachment hearings in the House of Representatives.

As this is written during the first week of October, economic stats are filtering in with the following worrisome messages:

- Manufacturing & construction activity in the USA is slowing

- The Farm economy has lost export markets and is slowing

- European, Chinese and Japanese economies are slowing

- Business confidence in the US is being hurt by the Trade War and political uncertainty

Given the string of bad news, it would be natural to expect a bear market to be well underway. Yet not only is there no such trend, many of our recommended holdings achieved new all-time price highs in September. Further, fixed income vehicles and funds have benefited from the determination of the Federal Reserve to manipulate interest rates as low as necessary to protect the current economic expansion, now a record ten years in duration.

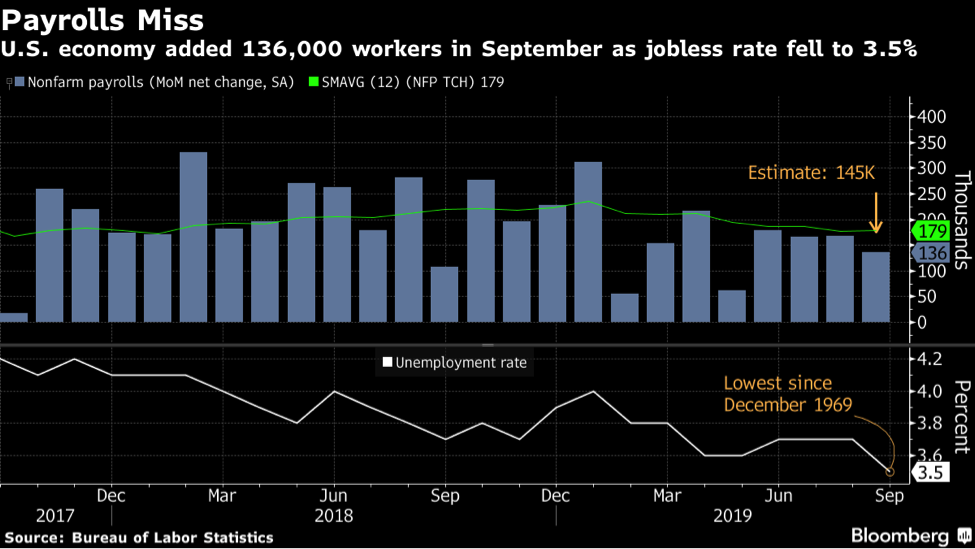

Perhaps the reason markets are holding up is historically high employment and healthy consumer confidence. For September, unemployment fell to a record low 3.5% although many in the media chose to highlight the fact that the pace of new hiring has slowed.

Source: Bloomberg.com

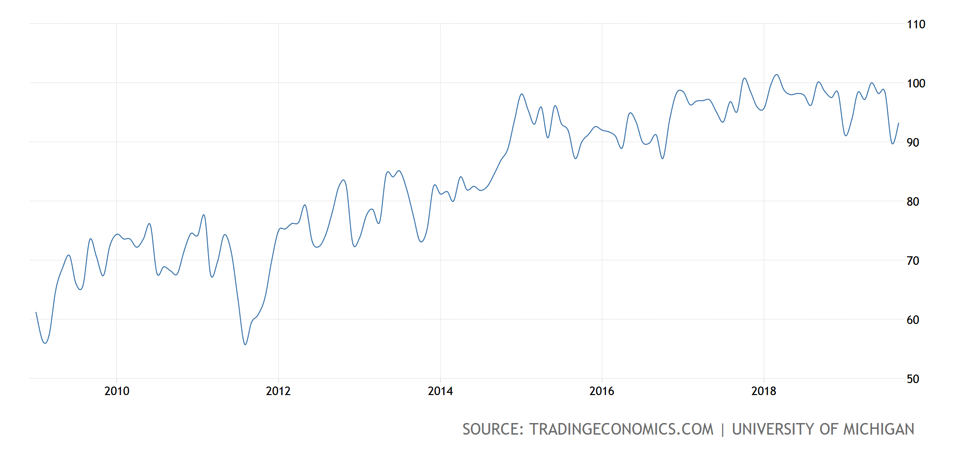

Since the U.S. economy is consumer driven, optimism or pessimism on the part of the everyday consumer is closely monitored. High employment rates translate into healthy consumer spending. Yet with September figures just out, it is clear there has been some softening of confidence. Over the past ten years, roughly the time of the current economic expansion, consumer confidence has fluctuated. Still the September figures do not yet present a worrisome picture.

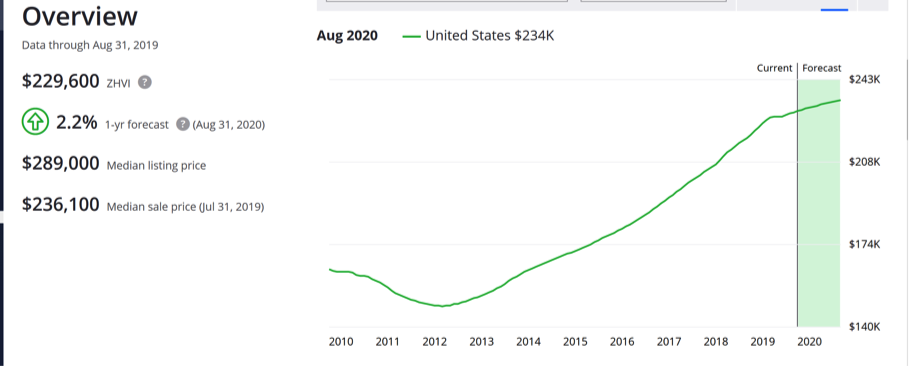

The number one source of wealth for Americans, their home value, has risen steadily since 2012. Zillow is, however predicting that growth in home values will slow to about 2.2% in the next twelve months. This may dampen consumer enthusiasm (the so-called “Wealth Effect”), but does this mean we will fall into an outright recession?

Source: Zillow.com

Undoubtedly, strength in stocks has also helped consumer attitudes, but now investor confidence is eroding, funds have flowed out of stocks for months now. Professional money managers are holding high amounts of cash and failed IPO’s (Uber, Peloton and We Work ), also suggest that investors are not willing to throw money at “story stocks”. This is a reassuring expression of investor behavior, because bear markets rarely begin during an environment of investor caution, rather, they arise out of speculative bubbles.

Many investors, particularly retirees, depend on income from their savings. Interest rates and yields on money market instruments that rose earlier this year are once again falling. This denies these folks some of their spending capacity, and so they seem to be willing to stretch for better returns from fixed income instruments. I am a bit concerned that some investors may not appreciate that leveraged loans from the private sector may be embedded in funds they believe to be bullet proof. A number of authorities, including members of the Federal Reserve Board of Governors have indicated confidence in our banking system, but remain cautious about the non bank lending, where “covenant light” borrowing is becoming the norm.

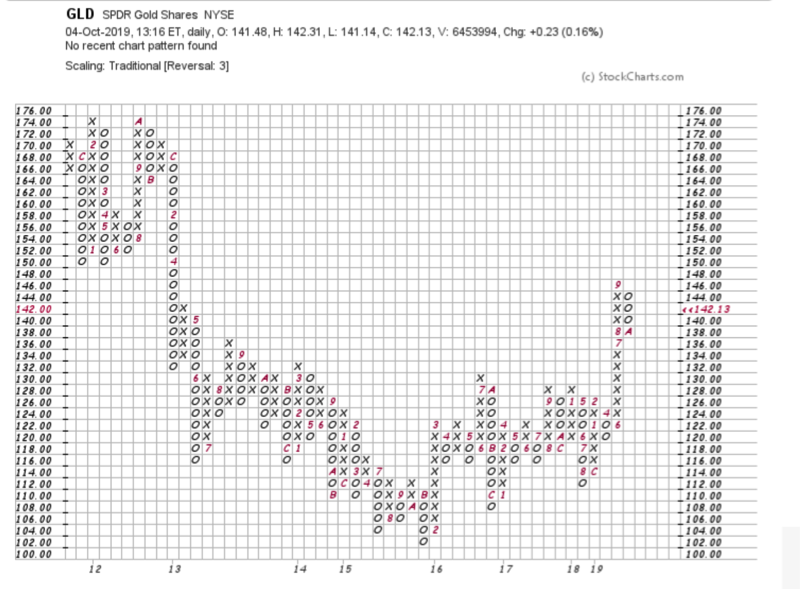

A major change in client portfolios was sparked when Gold emerged from a six-year bear market and base building in late July: I advocated for a cautious entry into the commodity, the first time clients have seen this holding in their portfolios in many years.

Source: stockcharts.com

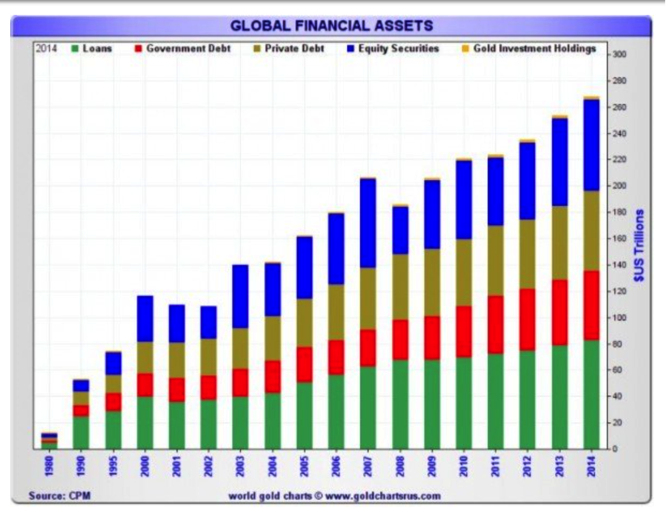

It is difficult to pin down what lays behind this meaningful price change. Is it prescience about the implications of ballooning Federal deficits? Monetarists will tell you that expanding the Fed’s balance sheet and money creation to service debt will lead to currency debasement, loss of confidence and runaway inflation. They argue for gold and other precious metals as a key hedge against this loss of currency buying power. The record for this claim is questionable. In fact, this break out in gold prices cannot be attributed to runaway inflation or lack of confidence in the dollar. Rather, some have postulated that with some $15 trillion of global fixed income investments offering negative interest rates (wherein the saver pays to park money at a bank), some money may be shifting to “real money” assets like gold, that if held personally, does not carry a cost to store. The chart below[1], suggests that gold’s value, relative to other financial assets is nearly insignificant (can you spot the gold colored sliver atop each bar in the chart?). If only a very small fraction of money held in stocks, bonds or certificates of deposit were to be shifted into gold, this alone could cause a price spike for the precious metal. Another factor is India, arguably the fasted growing economy in the world, and soon to be the most populous nation. Indians own more gold than any other nation. Each year’s Diwali festival, which is upon us, sees gifting of gold as a driver of demand. We suspect that rising Indian wealth has been a factor that has pressured prices upward.[2]

TFA’s allocation to gold is small, for most clients, 3% of portfolio value or less, but we feel this is a worthwhile diversification and one that should lower portfolio volatility slightly.

The Big Picture

Central banks across the planet seem to be trying to sustain economic expansion by pushing interest rates down. But they may be pushing on a demographic string. As populations in major nations age, those who control, directly or indirectly, most of the world’s wealth, are unlikely to drive a fiery economic expansion. Sub-2% growth in the USA may become the norm, as it has in Japan. As seen on the chart below, older people want their money in safe places, so a shift to short term, savings account-type investments is rising. By driving interest rates down, central banks hope to drive money into more productive investments such as long-term bonds, stocks, real estate projects, etc. But I suspect these efforts will be less effective than hoped because old people are unlikely to take a flyer on a startup or hand money over to a real estate developer to finance a new warehouse.[3] Further, the demand for money may be tepid as uncertainty leads businesses to defer new projects, equipment acquisitions and hiring plans. If few want to borrow money and fewer want to lend money, its hard to envision a new, hotter cycle of economic growth on the horizon, and yes, recession becomes a distinct possibility.

Chart source: Liz Ann Sonders blog post on Twitter.com

It is postulated by some that the surplus of conservative money seeking a safe haven could even lead to negative interest rates for US Treasury instruments. The implications for such an occurrence are disruptive, suggesting asset bubbles and acceptance of overly risky instruments by investors. But let us not get ahead of ourselves! Finally, an election year cycle has been accelerated with impending impeachment hearings. These hearings will add another layer of uncertainty to the uncertainty that any presidential election year brings to investor confidence. If markets can merely hold value and generate dividends over the next year, we would consider that a win. With volatility likely to increase in coming months, portfolio allocation continues to be driven by a desire to keep month to month fluctuations manageable. We believe that well-balanced portfolios holding high quality instruments will serve as a lifeboat in any storms that may lie ahead

[1] date we have not been able to confirm

[2] In late 2017 the Modi government shocked India’s population by issuing a new currency and forcing the underground economy into the open. Doubtless many Indians have lost confidence in paper money.

[3] Financial Times recently offered a view of this situation: https://www.ft.com/content/7ebfa850-bf2d-11e9-9381-78bab8a70848