After touching historic highs in mid-February, US stock indexes slumped, with most technology winners of the past three years falling into a meaningful correction. All told, it was a first quarter that began on a positive note as markets cheered what they hoped would be a Trump 2.0 administration focused on deregulation and tax cuts. It ended not with a bang, but a whimper. All three major indexes lost ground this quarter, with the Dow off 1.3%, the S&P 500 shedding 4.6% and the Nasdaq sinking 10.2%; the latter two snapped a five-quarter winning streak. [1]

The strongest two sectors were energy and precious metals. Our clients had exposure to both, plus the usual diversification into bonds, preferred stocks and “cash”. While nearly all clients saw a decline, it was considerably cushioned by diversification.

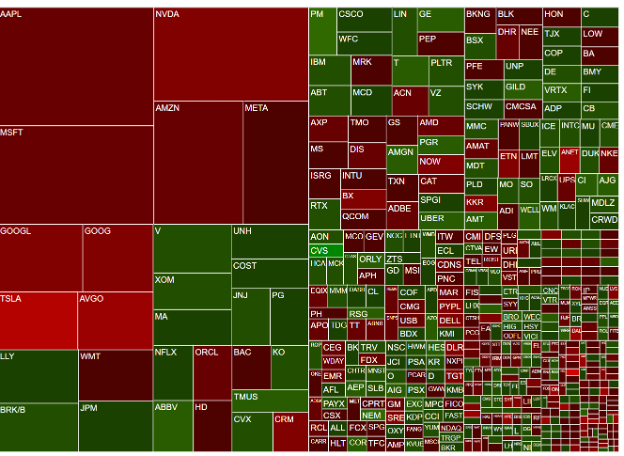

Below is a so-called “heat map” courtesy of Charles Schwab Institutional. Boxes in green indicate stocks that rose during the quarter, those in red stocks that fell. The relative size of the box indicates the degree of change. Plainly this quarter saw a correction for companies that were over loved.

This graphic shows performance of market sectors during the recent Quarter:

Source: Charles Schwab Institutional

It is always tempting to chase the hot dot, which is what investors were doing by mid-2024. The “Magnificent 7” stocks were certainly represented in most of our client portfolios, but did not dominate the mix. So, while the Mag 7 were soaring, Trusted Financial client accounts seemed to underperform. As a money manager one is always tempted to jump into whatever is popular at the moment. But I was in the trenches during the bearish 1970’s, the Crash of 1987, the Dot Com Bubble and the Great Financial Crisis of 2007-2009. The recollection of that pain is enough to dampen any tendency on my part to bet too heavily on any one sector. Clients like to see gains, yes, but they truly hate to experience losses. So, that is my focus: minimizing losses and living to fight another day.

Uncertainty Dragging

Few quarters have witnessed the whiplash seen in markets, driven by the advent of a new presidential administration and its no-holds-barred approach to remaking government. Many have been surprised at the extent of presidential power asserted by this administration and much of what has been initiated is being opposed in court. The climate for investors and business decision makers has rarely been so fraught and unpredictable.

The Trump administration’s efforts appear to focus on two paths: cut government’s bureaucracy and erect tariff walls to protect American workers and businesses.

Their approach (Musk and Department of Government Efficiency, DOGE) is a shock to government employees and agencies. Many feel it is a ham handed approach. Predictably, there is now a backlash from terminated federal employees. But even those in favor of rationalizing the bureaucracy wonder at the targets, as many cuts seem counterproductive: Centers for Disease Control?[2] National Weather Service? Bureau of Economic Statistics? Federal Aviation Administration? Likely Mr. Musk believes that efficient use of technology can offset reduced headcount in government. But some of these cuts to Federal agencies appear motivated not by a drive for efficiency but to satisfy an impulse to dismantle the government. Consider that the most efficient income producing agency, Internal Revenue, is slated to lose most if not all of the employees added by the Biden administration. Only history will tell if the approach has been successful or counter productive.

Our federal government is running massive deficits. While efforts to trim government waste and inefficiency are admirable, there appears to be a fantasy that taxes can be reduced in this environment and the lost revenue replaced by tariffs. Few if any economists agree.

Tariff Tribulations

Some of my favorite economists are Edward Yardeni, Mohammed El Erian and David Kelly. Kelly had this to say about Tariffs in a posting on March 3:

“The trouble with tariffs, to be succinct, is that they raise prices, slow economic growth, cut profits, increase unemployment, worsen inequality, diminish productivity and increase global tensions. Other than that, they’re fine.”[3]

Ed Yardeni, who was pleased by the presidential election, is beginning to sound a bit less sanguine about prospects for the economy:

“…we are reasonably sure that consumer spending will rebound in February and March.

Our bottom line is that we expect to see real GDP increase during Q1 between 1.5% and 2.5%. We are betting on the economy’s resilience. We are keeping the stagflation scenario in our what-could-go-wrong bucket with a 20% subjective probability.”

As for Dr. El Erian, he sums it up nicely:

“Some are wondering why we haven’t had more of a bounce in US equities after the partial rollback of tariffs on Canada and Mexico. I suspect part of the answer lies in the extent to which companies and households value the predictability and clarity of policies. As one CEO put it to me, “I just need a predictable operating environment to run my business effectively.”

Lastly, the most successful money manager of all time, Warren Buffet condemned tariffs by saying: “the tooth fairy doesn’t pay ‘em.”[4] Meaning tariffs will be a back door tax on consumers.

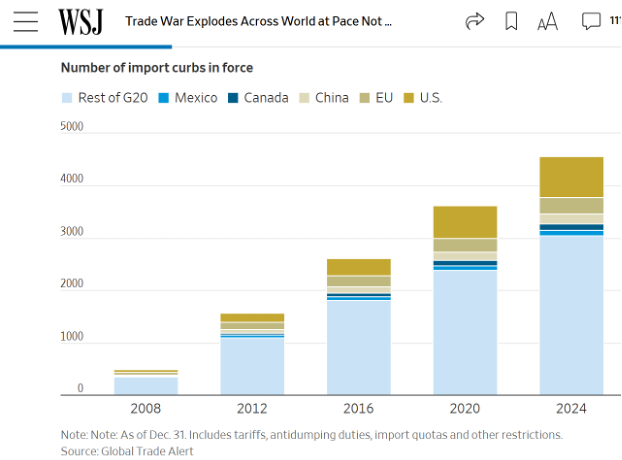

On March 25, 2025 the Wall Street Journal offered a worrisome overview of the effect of tariffs, and a graphic showing how they have been steadily rising globally, not just in the USA.

We have Something to Fear …Fear Itself

In mis-quoting Franklin D Roosevelt, I seek to highlight the great worry now upon us. The concern is paralysis. It’s not just tariffs and their deleterious effects that are concerning investors and business people. It is the unpredictability of the current chief executive. Over the last century the president of the United States has been granted extraordinary powers, powers that would not likely be approved by the generation of Americans who founded our republic. The capriciousness of King George III, as perceived by the American colonists, played a key role in fueling their rebellion. Though the term “mad” wasn’t widely used at the time (and his mental illness became more pronounced later), the king’s erratic and heavy-handed policies made him a symbol of tyranny in colonial eyes. Parliament, under George’s reign, imposed taxes like the Stamp Act and Townshend Acts without colonial representation. These taxes were passed and repealed seemingly on a whim, creating economic instability and political resentment. The “rebels” decided that a more democratic approach, while often clumsy and often slow, was preferable to having a monarch.

When the Rule of Law prevails there is some certainty about the future. Even if business people do not love new regulations or tax changes, they can at least count on them to remain in place for a time. This stability provides a basis for planning their future course of action, perhaps affording a way to work around the rules. When the macro economic environment becomes less certain because of overnight mandates or threats, followed by a sudden reversal, fear and paralysis can set in. This is climate we have today, oddly reminiscent of colonial days.

Historically it has been Democrats who imposed regulations and taxes, while Republicans usually sought to liberate business from burdensome requirements. During the 1980s and 1990s, it was primarily the Republican Party in the United States that embraced a Milton Friedman–style approach[5] to global markets—characterized by free-market capitalism, deregulation, privatization, low taxes, and open international trade.

Key examples include:

- Ronald Reagan’s administration (1981–1989): Reaganomics reflected many of Friedman’s ideas—slashing marginal tax rates, reducing the role of government in the economy, curbing inflation via tight monetary policy, and advocating for free trade.

- UK parallel – Margaret Thatcher’s Conservative Party: In the UK, Thatcher was equally influenced by Friedman and Friedrich Hayek, promoting free-market reforms, union restrictions, and privatization of state-owned enterprises.

Interestingly, in the 1990s, elements of this Friedman-esque market liberalism were also adopted by Democratic President Bill Clinton, who signed onto policies like:

- NAFTA (1994) – a hallmark of global free trade

- WTO entry and Permanent Normal Trade Relations with China

- Financial deregulation – including the repeal of parts of Glass-Steagall Act in 1999[6]

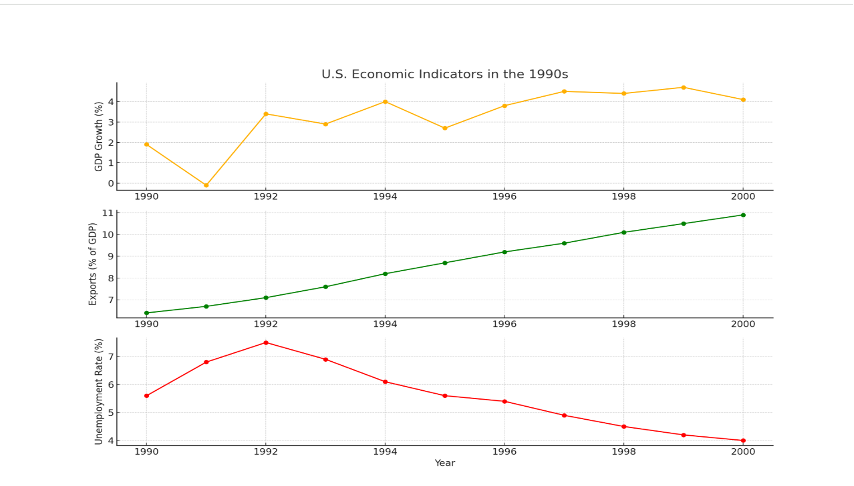

So, while the Republicans led the charge in aligning with Milton Friedman’s ideology in the ’80s, both major U.S. parties embraced aspects of global market liberalism during the 1990s. Of note, the US economy did well while free trade was spreading globally:

It is of particular interest that U.S. exports as a percent of GDP expanded during this period.

Globalization was good for large American corporations and for consumers with money in their pocket. However, it meant lost jobs for unionized workers in the private sector. The Trump administration, in seeking to protect American workers and businesses from foreign competition, is retreating from an approach that was once embraced by Republicans: a freer global market. Republicans of that era were no friend to trade unions. As the cost of manufacturing rose in the United States[i],countries with cheap labor, Mexico, Japan, and China replaced American plants in industries such as furniture manufacturing, textile and clothing manufacturing, television and electronics manufacturing. Steel and autos also have suffered from foreign competition. The winner in this has been consumers who can afford to buy things, such as Americans employed in “soft” industries like education, science, technology, finance and government. Those with low education or dated skills have suffered, so it appears that these folks cheer tariffs in the belief that bringing certain industries back to the United States will “make America great again.” Manufacturing has become global with multiple parts made in multiple nations. The idea of creating an island out of the United States and walling off the rest of the world is, frankly, impossible.

Hand in glove with protectionism goes anti-immigrant sentiment. Immigrants work cheaply and compete with American labor. This anti-immigrant cause used to be taken up by Democrats, but their attention has been drawn to environmental and social issues, while giving mostly lip service to protection for unionized workers. Donald Trump has grasped this, promising to help the little guy while cutting taxes and regulation for Big Business. In short, Trumpenomics is a populist approach, embraced by Billionaires!

Protectionism is clearly practiced by our international competitors. Government help has allowed foreign competitors, especially in Asia, to win market share from those domiciled in the USA. European regulators have continually harassed U.S. technology champions like Microsoft, Meta and Amazon. I recall discussing my annoyance at the admission of China to the World Trade Organization, some 25 years ago, at our annual client holiday luncheon. The concerns of people like myself have fully played out as China has made a national pastime out of stealing American technology and patents to produce copycat products they then sell to us at prices that make it hard for Americans to compete. American flags and July 4 holiday bunting found at Party City or Walmart, are mostly made in China. Peter Navarro, an economist who advocates for tariffs, seems to be sitting on the president’s shoulder, whispering the anti-free-trade mantra in Trump’s ear. I heard Navarro speak in 1998, and agreed then with his warnings about opening our markets to China. But his mercantilist, pro-tariff stance, now being applied to friendly nations like Canada has, in my opinion gone too far.

Tariffs seem appealing for those who forget history. The initiation of high tariffs in 1930 via the infamous Smoot-Hawley Act did little more than spark retaliation from other nations. Business activity cratered and a nascent recovery failed. The Great Depression, felt worldwide, not only led to suffering, but the unravelling of democracy in Europe, most notably in Germany.

Clearly government can play a positive role by subsidizing our companies with tax breaks and regulatory relaxation,[7] but will a trade war with the world be an effective approach to MAGA? The Biden administration included regulators who were not friendly to business. For example, as mentioned in previous reports, Lina Khan, the Biden administration’s head of the Federal Trade Commission made a habit of antagonizing our most important technology companies with new definitions of “fairness” in the marketplace. This was unhelpful and reflected an underlying Progressive suspicion of successful businesses. But, so far, Trump’s pattern of on-again-off again tariffs, accompanied by insulting language aimed at our allies, is perhaps even more unhelpful. Bullying certain industries that do not conform to the president’s views on social issues is a chilling authoritarian approach that is anti-capitalist. In my opinion, government needs to appreciate that native industriousness of American business and workers, not micromanage from D.C. Heavy handedness by politicians of both parties are not helping.

As clients know, I’ve invested their portfolios in the traditional oil and gas industry for over a decade, despite the unpopularity of the petroleum industry with many on the Left. Trump ran on advocacy for the oil industry with his phrase “drill, baby, drill.” Last week a confab of oil industry executives, who likely supported Trump’s re-election effort, were at the White House to support deregulation. What emerged however were complaints that steel tariffs will drive up their cost for drilling new oil and gas wells, making new wells in some cases unprofitable to drill!

Much of the current stock market correction in the United States is attributed to uncertainty. It is reasonable to give a new administration some time to settle in. Hoped for tax reduction and deregulation may well fall into place in the coming months. But if the current correction is reflected in slumping statistics for unemployment and business activity, it is highly possible that a course correction will emanate from the White House, or that even Congressional Republicans’ quiescence will end and push back in support for more normal, predictable behavior will emerge.

Discussion of Client holdings

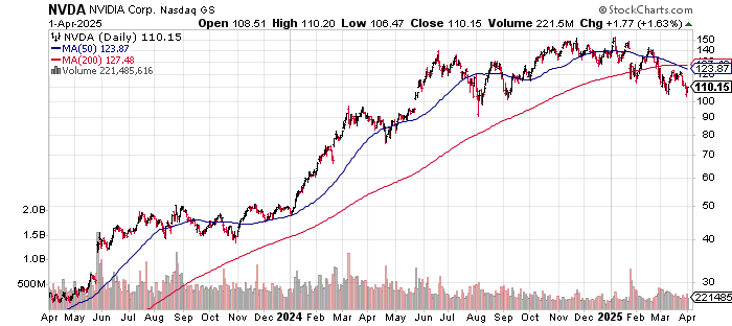

Nvidia stops to catch its breath

Nvidia, the darling of investors in the AI Era has slowly been losing value since late 2024. This despite cheer leading by its personable CEO Jensen Huang and revelations that sales are booming and ever faster chipsets are coming. The correction began this past quarter when Chinese company Deep Seek announced a cheaper way to power large language models, raising fears that demand for expensive artificial intelligence semi conductors would dwindle. This does not seem to have happened and further, competition for Nvidia chips has not emerged from any other company, like Intel (INTC) or Advanced Micro Devices (AMD).[8]

One problem for Nvidia is that a huge potential market, China, is not allowed to buy the most advanced Nvidia chips, a restriction that was imposed during the Biden administration. Meanwhile, plans for massive expansion of cloud farms (AKA data centers) here in the USA have apparently been delayed, amid questions about how rapidly artificial intelligence will be adopted.

Some equity exposure was reduced, largely in reaction to weakness in certain stocks as they reacted negatively to the chaotic political environment.

Sales during the quarter included trimming shares of Apple (AAPL) for those who appeared to have more than about a 5% allocation; exiting Broadcom (AVGO), whose shares weakened along with other semi conductor companies; exiting of Mathews India ETF (MINDX), based on fears of tariffs hurting imports into the USA. Finally, we closed the position in Arista Networks (ANET) taken in 2024. This company’s ethernet product, has seen disappointing sales, with dependence on few major customers, like META, a weakness. I should have dumped that one sooner.

Expanded Cash holdings

By and large, I’ve placed the proceeds of sales or redemption of preferred stock into overnight money market funds currently yielding a little over 4%. Recall these funds have a stable, non fluctuating share price of $1.00. As long term clients know, I’m happy to sit out uncertainty, keeping powder dry, collecting interest. If the current market weakness turns into a general rout, I’ll be looking for bargains to scoop up.

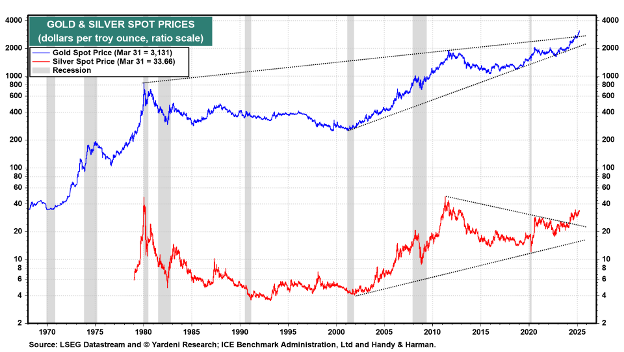

Gold Glitters

Late last year my technical indicators signaled significant buying of gold, so I decided to place small bets on the metal. A liquid vehicle for owning gold without actually holding the metal is SPDR Gold exchange traded fund (symbol GLD). So we put on a relatively small allocation of 3%. This is the first time we’ve owned gold in many years.Traditionally seen as a hedge against geopolitical and economic uncertainties, gold closed out its strongest quarter since 1986 on Monday, March 31 climbing to over $3,100/ounce, marking one of the most significant upswings in the precious metal’s history. I’ve not been a “gold bug” since the days of the fabulous gold bull market of the 1970’s, of which I was a part. In the mid 1970’s I believed that unrestrained printing of money would lead to a financial collapse and that owning traditional stores of value like gold and silver would provide salvation. Not exactly. Gold lost over half its value between 1980 and 1982 and then went nowhere for two decades. Gold is a commodity whose price depends on what people are willing to pay for it.[9] Industrial demand, important for metals like copper and iron is not a factor with gold. The metal finally began trending upward shortly after the turn of the century. This corresponded to a period when U.S. deficit spending began a sickening expansion. China and other central banks have been steadily increasing their holdings, as confidence the U.S. dollar is weakening.

Oil and Gas Holdings

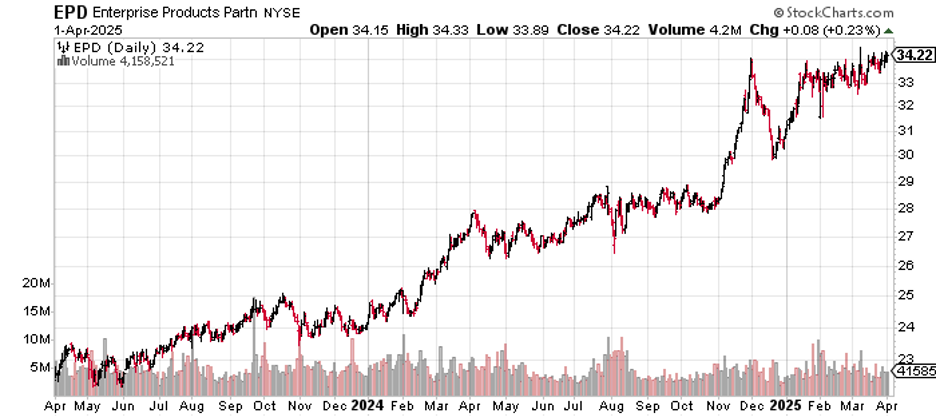

There is the strong international demand for natural gas, which has helped the share price of long time holding Enterprise Product Partners’ (EPD. With Europeans shying away from Russian gas, and America’s fracking boom unleashing gas trapped in shale rock deep below Texas, New Mexico and Wyoming to name a few, EPD with its vast network of gas pipelines and export terminals is positioned to profit from what I’ve long believed is a secular bull market.

A new position in Exxon-Mobil (XOM) was added to many client portfolios during the quarter. The stock has bounced around a bit, but by quarter end had become modestly profitable. Exxon Mobile recently purchased Pioneer Natural Resources, so now owns a large share of the prolific Permian Basin in west Texas and New Mexico. It also controls a huge deep sea field off the northern coast of South America. The company pays a healthy dividend, over 3.3% and is likely to raise it regularly into the future. However, unlike EPD which simply transports natural gas, as an upstream producer, XOM is sensitive to international oil and gas prices.

Summing it Up

In conclusion, we are in a period of heightened uncertainty. Diversified client portfolios have held up relatively well, and while the technology stock winners of last year are correcting, many holdings are doing well and a high allocation to conservative holdings leads me to feel confident that my long tested approach to portfolio diversification is appropriate for this time in history.

As always, I’m available to discuss your specific portfolio holdings and am always looking to hear your thoughts and objectives.

Gary Miller

[1] Source: Barron’s online 2025 03 31

[2] https://www.cnbc.com/2025/04/01/layoffs-begin-at-us-health-agencies.html

[3] https://www.linkedin.com/pulse/trouble-tariffs-david-kelly-lzbre/

[4] https://www.cnbc.com/2025/03/02/warren-buffett-calls-trumps-tariffs-a-tax-on-goods-says-the-tooth-fairy-doesnt-pay-em.html

[5] . Milton Friedman, an economist whose views gained popularity in the 1970’s and ‘80s postulated that all mankind benefits when there is free and open competition globally.

[6] I believe the repeal of Glass Stegall was largely responsible for the near collapse of the banking system in 2007

[7] Many states, like Texas sell themselves as attractive places to do business-witness the exodus of companies from high tax states like California and Illinois to more friendly venue. The Federal government bailed out our auto industry as well our banking and insurance giants during the Great Recession.

[8] https://www.barrons.com/articles/intel-ceo-compete-nvidia-ai-server-6d3da3c4?st=miDmiE&reflink=desktopwebshare_permalink

[9] Kind of like crypto currencies!

[i] This was due to strong labor unions and imposition of pollution control and product safety laws.